|

|

Post by Blitz on Aug 21, 2023 15:28:47 GMT -5

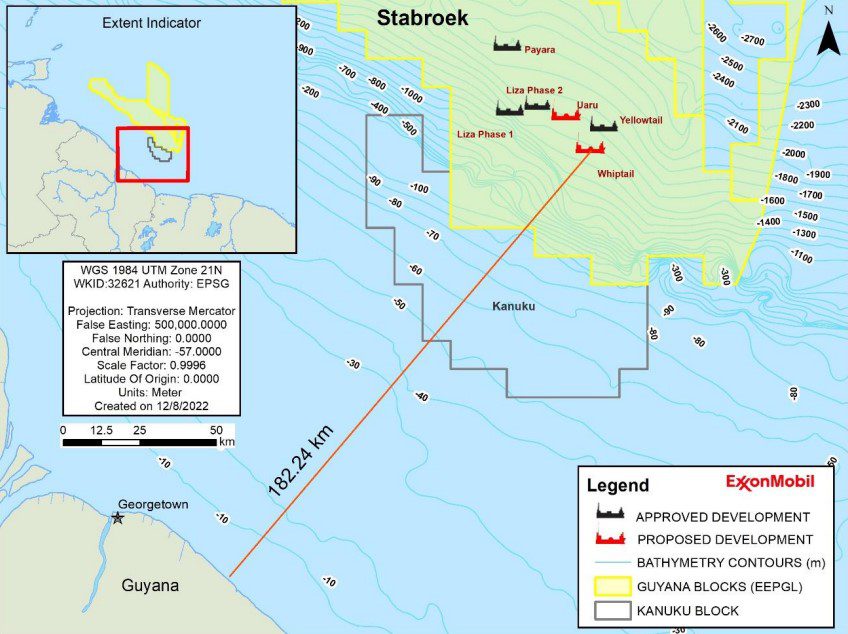

Exxon Proposes Sixth Oil Project in Guyana for $12.9 Billion brazilenergyinsight.com/2023/08/21/exxon-proposes-sixth-oil-project-in-guyana-for-12-9-billion/ (Reuters) Exxon Mobil Corp and partners plan to spend $12.93 billion to develop their sixth offshore oil project in Guyana, according to a filing published on Monday by the South American country. The floating production platform for the so-called Whiptail project would start operations in 2027 and bring the Exxon-led consortium’s oil output in Guyana over 1.2 million barrels per day (bpd). Guyana has emerged as the world’s fastest-growing new oil province in a decade with discoveries of more than 11 billion barrels of oil and gas. Exxon and partners Hess Corp and CNOOC Ltd now produce 400,000 bpd from two vessels and have said they could develop up to 10 offshore projects. Their production has brought $2.8 billion in direct revenue to Guyana and led to work for some 4,400 Guyanese. The Whiptail project outlined in the Environmental Impact Analysis made public on Monday by the government is similar to Exxon’s fifth project – Uaru – with output of 250,000 bpd and an upper production limit of 263,000 bpd. Exxon, Hess and CNOOC committed to spending $12.7 billion for Uaru earlier this year. The project does not plan to produce natural gas because studies indicated that any reduction in injected gas would result in reduced oil recovery, the filing said. The partners plan to drill up to 72 wells with development drilling scheduled from late 2024 through mid-2030. Installation of subsea components would begin in the second half of 2025 or early 2026, according to Exxon. The project is expected to employ up 540 people during the drilling and installation stage and from 100 to 180 people during production operations, Exxon said in the document to Guyana’s Environmental Protection Agency (EPA). |

|

|

|

Post by Blitz on Aug 22, 2023 6:41:06 GMT -5

Trying to read the tea leaves here and connect some dots... Guyana wants to speed up the "P" portion of E&P in their waters. Guyana asked XOM to give back some offshore blocks because they thought XOM had too many blocks moving too slow. XOM wants to keep as many wells as possible in order to prevent some of those give backs and keep that number as low as possible. So, XOM is going to be drilling more holes faster into the seafloor. As far as I can tell, it takes around 60 days to drill a deepwater well if all goes right. That's almost 12 years of work for one drillship. That's too long for Guyana to wait. Guyana has estimated they will 6-7 more drillships. I'm thinking XOM will need more drillships to keep more blocks. That will increase the number of drillships needed in an already tight market... meaning dayrates are going up and paid reactivations will begin sooner rather than later. And now this... ExxonMobil’s Whiptail project sets sights on 72 wells to propel oil output surge By OilNOW - August 21, 2023 oilnow.gy/featured/up-to-72-wells-targeted-for-exxons-massive-sixth-stabroek-block-development-as-eia-submitted-for-review-approval/ ExxonMobil’s Whiptail project is slated to target up to 72 wells to develop the fields. This was outlined in the Whiptail Environmental Impact Assessment (EIA) submitted to Guyana’s Environmental Protection Agency (EPA) for review and approval, on August 20. “…EEPGL has identified the presence of multiple reservoirs of crude oil with an estimated recoverable resource of approximately 1.75 billion cubic meters (m3) of oil-equivalent resources in the eastern half of the Stabroek Block,” the EIA outlined. With it completed, there is now a 60-day period for perusal of the 3,600+ page document by the public where they can make written submissions, citing any concerns they may have. The Whiptail development will be located 195 kilometers northeast of Guyana’s capital Georgetown. Along with the 72 wells being drilled (including production, water, and gas injection wells), the project also entails installing and operating subsea umbilicals, risers and flowlines, a floating production vessel, and decommissioning. Onshore logistical support facilities and marine/aviation services will be used to support each development stage. As with previous developments, Whiptail will also employ the use of onshore infrastructure – shore bases, warehouses, storage and pipe yards, fabrication facilities, fuel supply facilities and waste management facilities. Whiptail is expected to employ up to a peak of 540 people during the drilling and installation stage and from 100 to 180 people during the production operations stage. Production levels at Whiptail are expected to be 250,000 barrels of oil per day (bpd). The FPSO will be used to produce the crude, with two million barrels of oil storage capacity. The project will offload crude to a tanker, every three to six days during peak production. Exxon has signed a memorandum of understanding with SBM Offshore, for the construction of a multi-purpose floater hull. First oil is expected between the fourth quarter of 2027 and the second quarter of 2028, for at least 20 years. The project’s gas production capacity will be between 400 million and 640 million standard cubic feet per day (mscfd). ExxonMobil does not plan to export the gas. It has proposed using some for fuel for the project, then reinjecting the rest to maintain reservoir pressure and improve oil recovery. Whiptail is the last project on Exxon’s list of six to come online by 2027 in the Stabroek Block. While the goal for this milestone was 1.2 million bpd, Whiptail will take production capacity to more than 1.3 million bpd. |

|

|

|

Post by Blitz on Aug 22, 2023 6:59:25 GMT -5

This dovetails with the articleabove... Exxon’s 6th Stabroek Block project to cost almost US$13 billion OilNOW - August 22, 2023 oilnow.gy/featured/sixth-stabroek-block-project-whiptail-to-cost-us12-9-billion-eia/ExxonMobil Guyana’s next targeted development – Whiptail – is expected to cost US$12.933 billion (GY$2.690 trillion) according to the project’s Environmental Impact Assessment (EIA). Exxon said it has not yet made a final investment decision (FID) on Whiptail and is “continuing to evaluate cost considerations” during its development process. Its Whiptail development will be tapping into three massive reservoirs – Whiptail, Pinktail, and Tilapia. The Whiptail- 1 discovery was announced in July 2021. The Whiptail-1 well encountered 246 feet (75 meters) of net pay in high-quality oil-bearing sandstone reservoirs and was drilled in 5,889 feet (1,795 metres) of water. A discovery was also announced at Whiptail- 2 in July 2021. The Whiptail-2 well encountered 167 feet (51 metres) of net pay in high-quality oil-bearing sandstone reservoirs. Whiptail-2 was drilled in 6,217 feet (1,895 metres) of water. Reports indicate that Exxon is expecting to issue an FID by October. The Guyana government back in February had budgeted GY$100.7 million (US$483,000) to review Whiptail’s field development plan (FDP). This will be Exxon’s sixth development in the Stabroek Block. In total, there is potential to place 10 floating, production, storage, and offloading vessels at Stabroek. ExxonMobil has a 45% operating stake in the Stabroek Block, while Hess has 30% and CNOOC has 25%. |

|

|

|

Post by psvwordtkampioen on Aug 22, 2023 9:42:36 GMT -5

Something does not add up. 1.75 billion m3 = 1.75 E9 * 1000 = 1.75E12 l -> 1.75E12 l /119 l/barrel = 14 billion barrels.

14 billion barrels / 13 billion dollars is 1 dollar/barrel.

At $80/barrel, they would be making a *$%&load of money.

|

|

|

|

Post by Blitz on Aug 22, 2023 10:11:43 GMT -5

Something does not add up. 1.75 billion m3 = 1.75 E9 * 1000 = 1.75E12 l -> 1.75E12 l /119 l/barrel = 14 billion barrels. 14 billion barrels / 13 billion dollars is 1 dollar/barrel. At $80/barrel, they would be making a *$%&load of money. I think you got *$%&load of money part correct. Ship load of money in costs and ship load of profits. Breakeven oil price is $25 - $35/bbl offshore Guyana. Does this help your formula make more sense?  |

|

|

|

Post by bjspokanimal on Aug 22, 2023 12:41:24 GMT -5

Those ultra-low production costs in Guyana are the result of Exxon getting

the Stabroek block before Guyana wised up and ended it's ultra-low profit-sharing

and royalty scheme in favor of one more in line with other countries.

That's why Exxon et-al are pedal to the metal to develop as much as possible

before time runs out and any portion of the block reverts back to Guyana to

re-auction at the much higher lease rates. Frankly, I'm surprised they've

committed as much to the Permian shale as they have instead of putting everything

they've got into Stabroek. Their Permian holdings aren't going anywhere while

they put money into Stabroek.

|

|

|

|

Post by Blitz on Aug 22, 2023 16:14:57 GMT -5

After just announcing a $13B, 72 well, 6th project, XOM is adding project #7... to help XOM find the most productive areas with the highest potential... so that they only give back lower potential blocks to Guyana. And now this... Excerpt: ExxonMobil keeps on drilling with eyes on new Guyana cluster Company is considering a potential Fangtooth-Lancetfish cluster in the Stabroek block 22 August 2023 - By Fabio Palmigiani in Rio de Janeiro www.upstreamonline.com/exploration/exxonmobil-keeps-on-drilling-with-eyes-on-new-guyana-cluster/2-1-1504886US supermajor ExxonMobil is conducting a new range of appraisal activities offshore Guyana in a bid to de-risk a potential deep-water cluster that may turn out to be the seventh production development in the Stabroek block. |

|

|

|

Post by psvwordtkampioen on Aug 24, 2023 8:57:33 GMT -5

Are you implying the costs are indeed around 1$/barrel, but it gets up to $25-$30 barrel because of royalties?

|

|

|

|

Post by psvwordtkampioen on Aug 24, 2023 8:59:03 GMT -5

Those ultra-low production costs in Guyana are the result of Exxon getting the Stabroek block before Guyana wised up and ended it's ultra-low profit-sharing and royalty scheme in favor of one more in line with other countries. That's why Exxon et-al are pedal to the metal to develop as much as possible before time runs out and any portion of the block reverts back to Guyana to re-auction at the much higher lease rates. Frankly, I'm surprised they've committed as much to the Permian shale as they have instead of putting everything they've got into Stabroek. Their Permian holdings aren't going anywhere while they put money into Stabroek. ... and this implies they have to be racing to get those wells drilled before somebody else picks up the drill ships, or not? |

|

|

|

Post by Blitz on Aug 24, 2023 13:11:28 GMT -5

Are you implying the costs are indeed around 1$/barrel, but it gets up to $25-$30 barrel because of royalties? No. |

|

|

|

Post by bjspokanimal on Aug 24, 2023 18:41:01 GMT -5

ExxonMobil may be considering rig availability when speeding up Stabroek block development but that certainly isn't the #1 factor driving the haste.. not even close. The urgency is to find and FID prospects before portions of Stabroek block run out of time on their leases and those portions have to be relinquished back to the government. My point was that Permian don't have nearly as narrow of time constraints to develop them, since the purchase of drilling rights or outright land purchases there aren't nearly as urgent to be developed as Stabroek is. But I'm sure ExxonMobil knows better than I what the priority tradeoffs are.

|

|

|

|

Post by Blitz on Aug 24, 2023 20:29:16 GMT -5

Those ultra-low production costs in Guyana are the result of Exxon getting the Stabroek block before Guyana wised up and ended it's ultra-low profit-sharing and royalty scheme in favor of one more in line with other countries. That's why Exxon et-al are pedal to the metal to develop as much as possible before time runs out and any portion of the block reverts back to Guyana to re-auction at the much higher lease rates. Frankly, I'm surprised they've committed as much to the Permian shale as they have instead of putting everything they've got into Stabroek. Their Permian holdings aren't going anywhere while they put money into Stabroek. ... and this implies they have to be racing to get those wells drilled before somebody else picks up the drill ships, or not? Along with what Spok said, in my tiny brain, it implies that XOM knows they are sitting on a black gold mine. Guyana has also wised up. Guyana knows that they have a black gold mine too. Everyone knows the ESG woke folks are trying to mandate an end to black gold. Self-interest was guiding XOM… not Guyana’s interests. To exploit the black gold before it will be mandated out of existence, Guyana got impatient and more educated on what they had and how to run the show to their advantage and not XOM’s advantage. So, Guyana essentially told XOM they had to return some blocks that were going under-explored, under utilized, and therefore non-productive and not monetized. After the come to Jesus meeting between XOM and Guyana, XOM is told they must give back acreage not being used. So, if you are XOM what do you do? You can’t piss off Guyana and kill the goose that lays your black gold eggs, so you drill holes. The good holes you keep the dry holes you give give back. That’s not going to be 100% accurate, but it’s at least a more educated guess to determine what to keep and what to return. As for drillships, their cost compared to profits is like barrel of fresh water dumped in the ocean. It does not change the salinity one bit or raise sea water levels. Now, throw in Covid lockdowns destroying oil demand, low oil prices, demonization of reliable fuels by ESG fairy tales related to green unreliable energy, and false assumptions predicting grids powered by unreliable green power sources, big oil underspent on new wells and support infrastructure. Big oil was reluctant to spend on E&P for a demonized power source and under-invested. So, because offshore projects have very long lead times. Big oil decided to wait and see. During the wait and see period, drillship fixture barely cover fixed cost breakeven rates. The company letting a tender was getting dirt cheap rates. Drillship companies were going bk. Big oil dictated terms. Now the tables have turned, but it takes time to establish a new base for dayrate expectations. That is an ongoing process. India’s ONGC is an example of expectations that derailed but are finding a new base. They failed to budget for rising drillship dayrates. That forced them to tender for one drillship instead of two. That said, I know big oil can count. They can count world totals of floaters. They can count how many profitable holes they need to drill. They can count barrels of oil needed to power grids, power ICE vehicles, and supply chemicals for products made from oil. It just takes time to reset baseline expectations and rework budgets. Don’t forget after the last reset, RIG had drillships with $600K dayrate handles. The end of those contracts was this year and last year. Those days are coming again. |

|

|

|

Post by psvwordtkampioen on Aug 24, 2023 21:50:23 GMT -5

This all makes perfect sense.

|

|

|

|

Post by Blitz on Aug 25, 2023 8:01:01 GMT -5

This all makes perfect sense. YAY!  |

|

|

|

Post by lr on Aug 25, 2023 8:25:56 GMT -5

Great analysis

|

|

|

|

Post by bjspokanimal on Aug 25, 2023 12:41:17 GMT -5

One footnote I would add to this, is that developing countries all over

the world that have proven or prospective oil reserves are nervous about

all the (mostly woke) talk about "peak oil". It makes them worry that

their oil could become stranded over the next few decades and hastens

their actions toward getting it developed and flowing sooner.

There are multiple things I like about Transocean right now but, strangely,

one of the main ones is the positive influence that I think the energy

transition toward renewable energy is having.

The energy transition is having the dual benefit of creating urgency to

develop oil resources, as I mention above, and it is also causing deepwater

drillers to scrutinize the economics of newbuild rigs more than before

since a brand new drillship with a lifespan of as much as 50 years may not

have a good payback if the energy transition begins to lessen demand for oil markedly

10 to 15 years from now.

Personally, as a disciple of Transocean's slide #4 from last January's slide

presentation (among other illustrations), I'm less concerned about oil demand

20 years from now than most people are. But there's no denying that there's far

more uncertainty in the industry than there was in previous drilling up-cycles

and uncertainty always impacts major investment decisions.

I would add that with 12, cold-stacked drillships still out there and 4 stranded

drillships still owned by the shipyards they sit in, nobody's going to consider paying

over $1 billion for a pure-newbuild drillship until all those idle assets are working

and deepwater drilling CEOs get a feel for where the cycle is and the demand is

for rigs at that time. That "time" is still many years off, IMO (and the opinion of

Noble's CEO) so there's little question in my mind that we won't see any newbuild

drillships this decade. Given the current sold-out situation with H.E. semis, it is

possible that one or 2 could get build before 2030, however.

|

|

|

|

Post by Blitz on Aug 25, 2023 13:17:14 GMT -5

One footnote I would add to this, is that developing countries all over the world that have proven or prospective oil reserves are nervous about all the (mostly woke) talk about "peak oil". It makes them worry that their oil could become stranded over the next few decades and hastens their actions toward getting it developed and flowing sooner. There are multiple things I like about Transocean right now but, strangely, one of the main ones is the positive influence that I think the energy transition toward renewable energy is having. The energy transition is having the dual benefit of creating urgency to develop oil resources, as I mention above, and it is also causing deepwater drillers to scrutinize the economics of newbuild rigs more than before since a brand new drillship with a lifespan of as much as 50 years may not have a good payback if the energy transition begins to lessen demand for oil markedly 10 to 15 years from now. Personally, as a disciple of Transocean's slide #4 from last January's slide presentation (among other illustrations), I'm less concerned about oil demand 20 years from now than most people are. But there's no denying that there's far more uncertainty in the industry than there was in previous drilling up-cycles and uncertainty always impacts major investment decisions. I think when Poo-tin proved he'd lost mind by invading Ukraine, it also proved the world needs many sources for reliable power. If you don't you're going to left out in the cold and paying very high prices to get warm, drive vehicles, and power grids. So, the good part of the invasion was Poo-tin provided real world proof that exposed ESG mandates for eliminating hydrocarbons were fairy tales. Too many people, countries, investment firms, and energy related corporations were drinking the Kool Aid. Since then, energy security (ES) has become the top priority. This brought profits back into the picture due to reliable energy supply shortages. So much, profit the ESG crowd asked for windfall taxes and big oil paid out big dividends and increased infrastructure spending. Flush with huge profits and a much more clear path related to reliable energy needs, big oil got comfortable with higher fixture rates. My guess, in private, many of the world's power brokers might even be saying that energy security is more important than flying their jets to ESG parties all over the globe. They know ESG energy plans and timelines are wishful thinking. So, 'ES' has replaced ESG's 'Environmental and Social'. This means drill baby, drill for ES... and as you say, Spok, no new drillships are being built making RIG's fleet even more valuable. Floaters are so valuable and with so much less Social stigma, big oil will pay for unstacking and dayrates will hit $600K/day... most likely late next year. |

|

|

|

Post by psvwordtkampioen on Aug 25, 2023 23:23:19 GMT -5

One footnote I would add to this, is that developing countries all over the world that have proven or prospective oil reserves are nervous about all the (mostly woke) talk about "peak oil". It makes them worry that their oil could become stranded over the next few decades and hastens their actions toward getting it developed and flowing sooner. There are multiple things I like about Transocean right now but, strangely, one of the main ones is the positive influence that I think the energy transition toward renewable energy is having. The energy transition is having the dual benefit of creating urgency to develop oil resources, as I mention above, and it is also causing deepwater drillers to scrutinize the economics of newbuild rigs more than before since a brand new drillship with a lifespan of as much as 50 years may not have a good payback if the energy transition begins to lessen demand for oil markedly 10 to 15 years from now. Personally, as a disciple of Transocean's slide #4 from last January's slide presentation (among other illustrations), I'm less concerned about oil demand 20 years from now than most people are. But there's no denying that there's far more uncertainty in the industry than there was in previous drilling up-cycles and uncertainty always impacts major investment decisions. I would add that with 12, cold-stacked drillships still out there and 4 stranded drillships still owned by the shipyards they sit in, nobody's going to consider paying over $1 billion for a pure-newbuild drillship until all those idle assets are working and deepwater drilling CEOs get a feel for where the cycle is and the demand is for rigs at that time. That "time" is still many years off, IMO (and the opinion of Noble's CEO) so there's little question in my mind that we won't see any newbuild drillships this decade. Given the current sold-out situation with H.E. semis, it is possible that one or 2 could get build before 2030, however. If we connect the lack of new drill ships and semis with the urgency to drill + a steady stream of new deep water discoveries, something has to give. I don't have the overview to put supply and demand together, but my gut feeling says that at some point, something has to give. |

|

|

|

Post by Blitz on Aug 26, 2023 6:45:15 GMT -5

One footnote I would add to this, is that developing countries all over the world that have proven or prospective oil reserves are nervous about all the (mostly woke) talk about "peak oil". It makes them worry that their oil could become stranded over the next few decades and hastens their actions toward getting it developed and flowing sooner. There are multiple things I like about Transocean right now but, strangely, one of the main ones is the positive influence that I think the energy transition toward renewable energy is having. The energy transition is having the dual benefit of creating urgency to develop oil resources, as I mention above, and it is also causing deepwater drillers to scrutinize the economics of newbuild rigs more than before since a brand new drillship with a lifespan of as much as 50 years may not have a good payback if the energy transition begins to lessen demand for oil markedly 10 to 15 years from now. Personally, as a disciple of Transocean's slide #4 from last January's slide presentation (among other illustrations), I'm less concerned about oil demand 20 years from now than most people are. But there's no denying that there's far more uncertainty in the industry than there was in previous drilling up-cycles and uncertainty always impacts major investment decisions. I would add that with 12, cold-stacked drillships still out there and 4 stranded drillships still owned by the shipyards they sit in, nobody's going to consider paying over $1 billion for a pure-newbuild drillship until all those idle assets are working and deepwater drilling CEOs get a feel for where the cycle is and the demand is for rigs at that time. That "time" is still many years off, IMO (and the opinion of Noble's CEO) so there's little question in my mind that we won't see any newbuild drillships this decade. Given the current sold-out situation with H.E. semis, it is possible that one or 2 could get build before 2030, however. If we connect the lack of new drill ships and semis with the urgency to drill + a steady stream of new deep water discoveries, something has to give. I don't have the overview to put supply and demand together, but my gut feeling says that at some point, something has to give. The 'give' is rising dayrates... and we've seen that happening. Dayrates have doubled over the last year and half. the 'giving' will continue until every drillship is contracted. Also, I expect most new contracts for drillship will drift toward long term fixtures in order to guarantee availability. |

|

|

|

Post by bjspokanimal on Aug 26, 2023 19:13:45 GMT -5

The overview to evaluate the supply and demand of floating drilling rigs is just to understand these elements: 1) dayrates.. they are rising as more and more oil/gas companies vie for fewer and fewer available rigs. 2) Active rig utilization.. this is how you gauge near-term supply as H.E. semis are now sold out through next April and drillship utilization is above 95%. 3) Stacked and stranded rig inventory.. floaters in this state are rapidly declining with just 12 cold-stacked and 4 stranded drillships remaining. Transocean owns 8 of the 12 cold-stacked drillships. 4) Oil company budgets for Deepwater E&P.. Steadily rising since mid-2021 and the proportion of Deepwater spending vs shallow water or onshore continues to increase. 5) FPSO orders and construction.. FPSOs are needed to Produce, Store and Offload Deepwater oil. The more FPSOs ordered, the more Deepwater oilwells must be drilled to provide oil and gas to them.

|

|

|

|

Post by psvwordtkampioen on Aug 26, 2023 21:52:25 GMT -5

Transocean has about 7 billion in debt. It has 728,000,000 stock, worth $7.71/stock = 5.2 billion dollar. Adding the two: $12 billion. It has 43 drills ships / semis, 12 of them inactive. This means roughly $330 million per active vessel or $260 million per active + inactive vessel. Using the $330M/vessel, at an average day rate of $500k and ignoring payment for the crews, the investment on all vessels can be returned in less than 2 years. I guess we all agree the stock price is too low, but what is preventing the stock price from not gaining more momentum?

|

|

|

|

Post by Blitz on Aug 27, 2023 7:59:46 GMT -5

Transocean has about 7 billion in debt. It has 728,000,000 stock, worth $7.71/stock = 5.2 billion dollar. Adding the two: $12 billion. It has 43 drills ships / semis, 12 of them inactive. This means roughly $330 million per active vessel or $260 million per active + inactive vessel. Using the $330M/vessel, at an average day rate of $500k and ignoring payment for the crews, the investment on all vessels can be returned in less than 2 years. I guess we all agree the stock price is too low, but what is preventing the stock price from not gaining more momentum? People are risk averse. The masses would rather wait to buy a stock until most of the risk is gone. By the time most of the risk is gone the stock's price has already made its biggest and quickest percentage gains. As risk diminishes, more and more people jump on the bandwagon. That is happening with RIG, just not at the pace we would like. 'We', on this forum, know the supply and demand dynamic is working in RIG's favor. Most investors don't 'drill down' far enough to know the numbers you've posted. They are just waiting for more fixtures with longer contracted time periods, with higher dayrates, and customer-paid reactivations. That makes RIG more predictable. It's easy to do the math for an XOM 5-year, $500K dayrate, with a customer-paid reactivation. When Shell, Chevron, TotalEnergies, and ONGC do the same, the math gets easier. As the math gets easier the risk comes off. That de-risking process is happening. Since I first bot RIG, the stock has gone up 7X. Dayrates will continue to rise and when RIG gets just one customer-paid reactivation, the risk averse will see that speculation regarding customer-paid reactivations has turned to reality. People will see those idle floaters will go from liabilities costing RIG money, to monetized assets making RIG money. As that happens the RIG bandwagon will become very crowded raising the stock price. It just takes time for the lemmings to jump on. |

|

|

|

Post by bjspokanimal on Aug 27, 2023 15:20:20 GMT -5

Transocean has 39 rigs, not 43... 29 ultra-deepwater and 10 harsh environment. Also, a hypothetical $500k (future) average dayrate is revenue, not a return on assets. From revenue must come costs, both operating costs and administrative costs. Non-cash costs like depreciation applies to earnings but not cash flow and EBITDA. In the end, it would take FAR longer than 2 years to pay for the company's fleet at an average dayrate of $500k per day, but then, drillships and h.e. semis have useful lives of over 40 years.

|

|