|

|

RIG

Apr 25, 2020 8:29:07 GMT -5

Post by Blitz on Apr 25, 2020 8:29:07 GMT -5

Well, drilling down on this ...  ... you've defined your total risk to be around $1 buck. So, I'm telling you, there's a chance at a multi-bagger ... |

|

|

|

RIG

Apr 27, 2020 9:35:22 GMT -5

Post by redbullnvodka on Apr 27, 2020 9:35:22 GMT -5

Looks like I was at least a day early.

|

|

|

|

RIG

Apr 27, 2020 9:46:27 GMT -5

Post by Blitz on Apr 27, 2020 9:46:27 GMT -5

I bot a little more today... Not sure if I have a case of dumb and dumber?

Earnings or lack thereof is later this week.

|

|

|

|

Post by bjspokanimal on Apr 27, 2020 17:30:44 GMT -5

The swoon today was a reaction to Diamond Offshore beginning a bankruptcy court reorganization.

It was anticipated after they missed a bond payment on April 15th. Diamond's credit rating was

at C+ whereas Transocean's is at B- but on watch for likely CCC+, as are some of their unsecured

notes.

|

|

|

|

Post by redbullnvodka on Apr 27, 2020 17:45:15 GMT -5

The swoon today was a reaction to Diamond Offshore beginning a bankruptcy court reorganization. It was anticipated after they missed a bond payment on April 15th. Diamond's credit rating was at C+ whereas Transocean's is at B- but on watch for likely CCC+, as are some of their unsecured notes. Would you say $20 oil in September is when you start getting concerned about RIG? |

|

|

|

Post by Blitz on Apr 27, 2020 18:31:52 GMT -5

With many in this space going bankrupt, I’m hoping RIG will get their business.

|

|

|

|

RIG

Apr 27, 2020 19:24:59 GMT -5

via mobile

Post by birdnest on Apr 27, 2020 19:24:59 GMT -5

Earnings for Wednesday after the bell will be interesting on how it trades. I can’t believe it’s in the .80’s.

|

|

|

|

Post by bjspokanimal on Apr 27, 2020 19:29:14 GMT -5

@ redbull et-al;

On the oil front: Everybody is cutting production now, including OPEC, because there's no place to store it

and there are no available tankers or pipeline capacities. Supply will equal demand by next week... either that

or producers will start dumping it into empty swimming pools.

Once we're at that point, producers that have closed down production to get us there will not re-start their

pump jacks until the price of oil rises to a level that allows them to break even. Very few producers can

produce profitably at prices below $30. If we get there quickly, major producers aren't likely to cease

development in multi-year, ultra-deepwater projects.

On the Transocean front: RIG was in good shape, relative to the other offshore drillers, before the Corona

Virus hit. RIG's EBITDA margin of 30% was the industry's best in Q4 and the company closed on around a dozen new

drilling contracts earlier in Q1. RIG also closed on a $750 million bond issue in January. RIG currently

has total debt of about $9.9 billion and net debt (debt less cash on hand) of about $6.9 billion. The new

bond issue yields 8%.

The thing to remember about ultra-deepwater drillers is that their clients are doing multi-year development

projects that have large payoffs in the out years. Large companies with both sh

ale and deepwater projects are

going to suspend the shale production first, before ending development of projects with future payoffs... especially

those with $billions already sunk into them. But they eventually will, if times get tough.

Diamond Offshore, which just filed for bankruptcy protection and reorganization, was in more precarious financial

shape than Transocean (C+ rated vs B- rated, but some of Transocean's unsecured

debt is CCC+ rated) and Diamond's rigs are older and less useful in the most promising,

deepwater plays. Seadrill, which has also reorganized once in bankruptcy court and may do so again, has the most

modern, overall fleet of deepwater rigs but went much further into debt to build them all so was in much more trouble

when the oil glut began back in 2014.

Transocean installed new management sometime around 2014/2015 and quickly started selling off or scrapping jackups and older

mid-water and deep-water rigs to essentially re-make the fleet and improve finances. Once done, they did a couple of

acquisitions and new-builds that are much more advanced than even Seadrill's relatively modern fleet... rigs that are

working and unlikely to be cancelled due to their unique capabilities. Revenues from these rigs will help Transocean

through the current industry crash, but not indefinitely, especially if contracts of lesser rigs are cancelled and the payouts

from their severance clauses aren't enough to shield RIG from a prolonged drilling slump.

Other things could happen. Transocean could be merged with another, relatively healthy player... like maybe Ensco, which is

also B- rated by S&P. Such a merger could be arranged via debtors with more favorable terms on the combined debt of the 2 companies.

RIG is also an attractive buyout, with a book value (calculated on it's favorably revamped fleet) of almost $20 per share,

but any acquirer would have to feel good about Transocean's liklihood to be a survivor for the next oil boom years from now.

If things are still bad late next fall, there would also likely be negotiations between RIG and it's lenders to modify

loan terms before bankruptcy is considered, and bankruptcy itself wouldn't actually shut down Transocean just as it hasn't

shut down Diamond, but would, rather, result in a reorganization whereby equity interests would cede some or much of those

interests to debt holders in return for relief and a strengthened balance sheet. As insolvency approaches for huge companies

like Transocean, debtors start thinking more like stockholders, because the company is worth more to them alive than dead.

Bottom line: True contrarian investing typically involves a struggle, and the fear involved with such a struggle is what

creates unbelievable value. There's risk, sure, but that's why I typically choose the best company in an industry whose

troubles I want to exploit... and Transocean is the biggest and best company in deepwater and harsh-environment contract drilling.

|

|

|

|

Post by bjspokanimal on Apr 28, 2020 12:11:38 GMT -5

One quick thing...

When looking at WTI crude these days, I would ignore the June contract as it's a bit messy.

At least one, major oil ETF (and likely more) are bailing on June and rolling over to future

months out of concern that June could likely do what the May contract did.

My rationale for that, is that currently, producers are closing down wells and that takes

time and a lot of selection and prep work. So, it's unlikely that production will decline

enough over the next few weeks to align sufficiently with demand from refiners and, since

oil storage facilities (and tankers) are virtually full, then there could again be no place to

put spot oil as the June contract expiration approaches and the contract could do what the

May contract did... go negative.

Further out, with the August WTI contract for instance, production curtailments are much more

likely to equal demand and demand could be slowly picking up. Thus, there will be places to put

crude that's produced and the price of crude will begin to reflect a more stable view of what

can be produced, and sold, with some semblance of economics.

So, looking at June WTI is kind of like looking at Golden Week in Macau and extrapolating Golden Week

GGR out to estimate GGR for the full year...

... it's unrealistic, and not an accurate reflection of normal GGR.

|

|

|

|

Post by Blitz on Apr 28, 2020 12:52:01 GMT -5

We’re about to find out if the cure for low oil prices is low oil prices.

|

|

|

|

Post by bjspokanimal on Apr 28, 2020 15:44:47 GMT -5

We’re about to find out if the cure for low oil prices is low oil prices. No worries. Very few producers can make a profit on oil under $25. The ones that can are almost entirely sovereign countries and most of those are in the middle east and they're hurting badly. The reason, is because they rely so heavily on profits from oil exports to run their countries. Saudi Arabia has a cost of production somewhere down around $6.00 per barrel, but right now they're borrowing money heavily to make up a huge budget deficit that's usually covered by much higher oil profits. This article was pretty good about how the producers are impacted: _________________________________________________________________________ Why The World Is Still Pumping So Much Oil Even As Demand Drops Away April 22, 20202:54 PM ET Camila Domonoske square 2017 CAMILA DOMONOSKE Twitter Producers have kept pumping oil, even if they're not making money, partly because wells — once shut down — can be difficult to get back up and running. Here, a pump jack operates at Willow Springs Park in Long Beach, Calif. Apu Gomes/AFP via Getty Images With the global economy in a pandemic-induced coma, the world just doesn't need a lot of oil. But oil is still flowing out of wells, and with nowhere else to go, it's filling up the world's storage tanks. The oversupply is so intense that this week U.S. oil prices briefly went negative. But why is that oil still flowing, anyway? Why don't producers turn off the spigot when demand falls? The short answer is that production is decreasing — just not fast enough. "The crude markets move in slow motion," says Bernadette Johnson, the vice president of market intelligence for Enverus. "So what we're seeing is almost a slow-motion train wreck." Crude in a pipeline can take weeks to reach its destination, which means oil purchased in mid-March could still be in transit in mid-April. This spring, the world completely transformed faster than some oil could finish that trip. And that's not the only source of delay. When demand plummets and prices drop, it takes time for oil producers to start turning off existing wells. Reducing output like that is known as "shutting in" production. "Shutting-in production is a very painful decision for an operator to make," Teodora Cowie, an analyst with Rystad Energy, writes. "Often the economics support running a well at a loss for a certain period of time rather than shutting down the project completely." As long as prices are greater than zero (an unusual disclaimer for these unusual times), a well will still bring in some money. And oil companies have fixed costs they have to cover. Even if they're taking a loss overall, it may be better to keep a well running than to bring in no money. They're also looking ahead to the future, when demand and prices are eventually expected to rebound. An oil well is not like a light switch you can flick on and off. A well that has been shut down can be hard to turn back on. Elizabeth Gerbel, CEO of EAG Services, an oil and gas consulting company, compares it to a bottle of soda. If you put the cap back on and store it in the fridge for a while, it will never be as bubbly as when you first cracked it open. Similarly, if you start pumping from a well, shut it down and try to get it running again, "it is almost guaranteed you will have to invest more money in the well to get it to produce at the same level," she says. And it's not just the physics of oil fields working against producers here. It's their legal contracts: They may have signed leases that require them to drill the land in question. "If you are forced to shut-in a lot, you technically can lose your lease to a competitor," Gerbel says. "And then you're going to have to buy them back." So even at very low oil prices — prices where oil producers clearly are unable to make a profit — they might opt to keep wells running now, to ensure they can operate those wells in the future. Eventually, very low prices make that untenable, and shut-ins do occur. Rystad Energy estimates that nearly 2 million barrels per day have been shut in already, mostly in Canada. And as the glut grows so intense that tanks, pipelines and ships run out of space, companies may be forced to shut in some wells that they would like to keep running, simply because there is nowhere they can immediately store their oil. There's another way that oil companies are reducing output: cutting back on new wells. Drilling a new well is expensive. Last month, the Dallas Fed Energy Survey reported that on average, U.S. firms need oil prices to be at least $49 per barrel to profitably drill a new well. The U.S. benchmark oil price is currently at less than $14 a barrel. So when prices drop, companies often move quite quickly to reduce drilling — well before they shut in existing production. The number of active drilling rigs has dropped to less than 440, according to data from Baker Hughes; it was at 825 a year ago. That means a drop in output, particularly for shale producers, which have to keep drilling new wells just to maintain existing production levels. But Johnson, of Enverus, notes that new shale wells can also be drilled and brought online unusually quickly. This means that while the shale industry — like the rest of the oil industry — is currently reeling, production could also come back quite quickly if demand returns. www.npr.org/2020/04/22/839851865/why-the-world-is-still-pumping-so-much-oil-even-as-demand-drops-away |

|

|

|

RIG

Apr 28, 2020 18:30:11 GMT -5

via mobile

Post by birdnest on Apr 28, 2020 18:30:11 GMT -5

Great info S...

I really enjoy reading your post on RIG. I know very little about this stock and probably shouldn’t have bought knowing very little. I’ve watched it for about a year and had to start buying when it dropped below $2. I’ve been buying all the way in the .90 ‘s - losing my ass..

I do appreciate everyone’s info on RIG though, I’m just learning. What do we think about tomorrow after the bell??

Transocean Q1 2020 Earnings Preview

Apr. 28, 2020 5:35 PM ETTransocean Ltd. (RIG)

Transocean (NYSE:RIG) is scheduled to announce Q1 earnings results on Wednesday, April 29th, after market close.

The consensus EPS Estimate is -$0.28 (+6.7% Y/Y) and the consensus Revenue Estimate is $796.59M (+5.6% Y/Y).

Over the last 2 years, RIG has beaten EPS estimates 38% of the time and has beaten revenue estimates 88% of the time.

Over the last 3 months, EPS estimates have seen 0 upward revisions and 17 downward. Revenue estimates have seen 3 upward revisions and 6 downward.

|

|

|

|

Post by Blitz on Apr 29, 2020 7:08:40 GMT -5

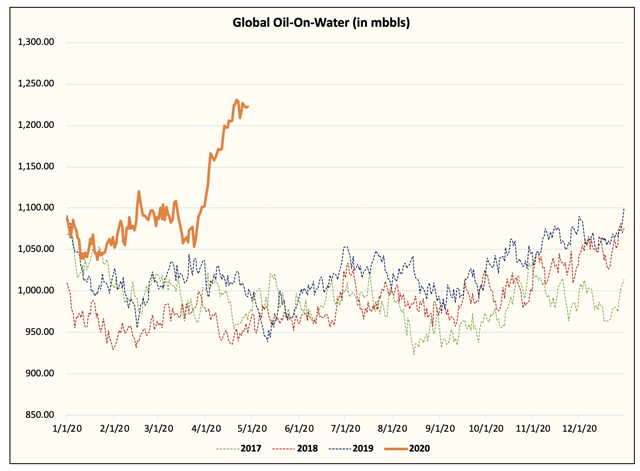

Oil: Global Crude Storage Builds In April Are Nowhere Near Analyst Estimates Apr. 28, 2020 8:56 PM ET|53 comments | Includes: AOIL, BNO, DBO, DTO, NRGD, NRGO, NRGU, NRGZ, OIL, OILK, OILX, OLEM, SCO, UCO, USAI, USL, USO, USOI, YGRN HFI Research The #1 oil and natural gas research service on Seeking Alpha. (17,479 followers) seekingalpha.com/article/4340763-oil-global-crude-storage-builds-in-april-are-nowhere-near-analyst-estimatesSummary Global crude storage onshore and on water has only built 260 million bbls MTD. This is an implied surplus of ~10 to ~11 mb/d, or less than half of the estimated surplus out there. April was a special month too since Saudis decided to shock the world by pushing production to ~12.3 mb/d. If we come out of this demand drop with less-than-expected inventory build, we could see global oil inventories reach normality by the end of the year. This would set up bullishly for oil prices in 2021. Last week, we wrote an OMF titled, "Global Oil Market - Let's Talk Data." The conclusion of that article was that global oil inventory builds have so far been well below the analyst demand destruction projections out there. And in today's report, we look to compare the actual data to the analyst estimates out there currently for global crude storage (not including products).  For the month of April, Energy Aspects is forecasting a ~20 mb/d crude storage build. This would be the equivalent of ~600 million barrels added to global crude storage. We looked at estimates from Kayrros and Kpler, and the figures for both onshore storage and oil-on-water are nowhere near the estimate of a ~20 mb/d oversupply in crude. Global Oil-on-Water  Source: Kpler From the end of March to today, global oil-on-water saw an increase of ~120 million bbls. For global onshore inventories, Kayrros pegs the increase month-to-date at ~140 million bbls. You combine the two and we get ~260 million bbls of storage increase. This is compared to the theoretical increase of ~480 million bbls as of April 24th. On an implied basis, we are talking about ~10 to ~11 mb/d of oversupply in crude versus the theoretical oversupply of ~20 mb/d. April was a special month too Now that you see the actual oversupply is less than half of the estimated oversupply out there, it's important to remember that April was a special month. It's a special month because Saudi decided to ramp up production to ~12.3 mb/d and boost crude exports to ~9 mb/d. This increase came at a time when the world is on total lockdown. So, the combination of demand hit and supply shock set the precedence for this oversupply both onshore and on the water. Why does this matter? How much we build in crude storage and oil products will determine the recovery shape of oil prices. If we build less than expected over the next 2-3 months, then it is very possible that global oil inventories are back to normal by the end of the year. This, combined with the global conventional capex falloff and decline in US oil production, will push the world into a material deficit in 2021. |

|

|

|

RIG

Apr 29, 2020 15:50:22 GMT -5

via mobile

Post by birdnest on Apr 29, 2020 15:50:22 GMT -5

RIG finally traded good yesterday and today. I thought maybe we had some momentum going into earnings but now under $1.00 after there report.

Transocean EPS misses by $0.02, misses on revenue

Apr. 29, 2020 4:27 PM ETTransocean Ltd. (RIG)3 Comments

Transocean (NYSE:RIG): Q1 Non-GAAP EPS of -$0.30 misses by $0.02; GAAP EPS of -$0.64 misses by $0.33.

Revenue of $759M (+0.7% Y/Y) misses by $37.73M.

|

|

|

|

Post by bjspokanimal on Apr 29, 2020 16:22:47 GMT -5

I can't fully concur with the seeking alpha author above. There are many disparities with on-the-water tanker storage with all of the geographic dispersion so I generally look to the source... how many empty tankers are idle and available in the Persian Gulf, and the answer is zero, which is why the Saudis/Kuwaitis/UAA/etc. have cut production ahead of the May 1 target. They can only load onto active tankers as they arrive. Re: storage, the author also leaves out "contracted" available storage capacity. So, that means that if Apache has no contracted capacity, they can't secure available empty storage that's contracted by Exxon-Mobil. Thus, Exxon can continue to produce and fill that capacity while Apache must shut-in some wells. I should add that the largest oil producers share 2, common practices: 1) They contract for a lot of storage space to get through times like these, and... 2) They are by far the most active in multi-year, ultra-deep water drilling projects like Transocean's rigs are suited for. It's another way that a company like Transocean is a bit more insulated from short-term, ups and downs in oil prices. Such spare, contracted capacity also gives the bigs more latitude to play with out months in futures. For example, Exxon can fill storage more sparingly for crude deliverable under the june contract and time it more for supply contracts that they let for July and August, thus securing higher prices for longer-dated crude and having a place to store it in order to target those higher prices. If that means the difference between having the funds, or not having them, to finance an ultra-deep water project, then it matters to us. Here is where I go for oil inventories. EIA (Energy Information Administration) is tops. API (American Petroleum Institute) is #2: www.eia.gov/petroleum/weekly/ |

|

|

|

Post by Blitz on Apr 29, 2020 17:06:01 GMT -5

seekingalpha.com/pr/17853452-transocean-ltd-reports-first-quarter-2020-resultsExcerpt: Transocean Ltd. Reports First Quarter 2020 Results Apr. 29, 2020 4:24 PM ETGlobeNewswireTransocean Ltd. (RIG) Total contract drilling revenues were $759 million (total adjusted contract drilling revenues of $807 million), compared with $792 million in the fourth quarter of 2019 (total adjusted contract drilling revenues of $839 million); Revenue efficiency(1) was 94.4%, compared with 96.2% in the prior quarter; Operating and maintenance expense was $540 million, compared with $575 million in the prior period; Net loss attributable to controlling interest was $392 million, $0.64 per diluted share, compared with net loss attributable to controlling interest of $51 million, $0.08 per diluted share, in the fourth quarter of 2019; Adjusted net loss was $187 million, $0.30 per diluted share, excluding $205 million of net unfavorable items. This compares with adjusted net loss of $263 million, $0.43 per diluted share, in the previous quarter; Adjusted EBITDA was $235 million, compared with adjusted EBITDA of $223 million in the prior quarter; and Contract backlog was $9.6 billion as of the April 2020 Fleet Status Report. STEINHAUSEN, Switzerland, April 29, 2020 (GLOBE NEWSWIRE) -- Transocean Ltd. (RIG) today reported net loss attributable to controlling interest of $392 million, $0.64 per diluted share, for the three months ended March 31, 2020.

|

|

|

|

RIG

Apr 29, 2020 18:04:55 GMT -5

Blitz likes this

Post by bjspokanimal on Apr 29, 2020 18:04:55 GMT -5

I had tomorrow on my calendar... forgot they do a late release then do the conference call at

6 am PDT tomorrow.

Nice to see their EBITDA margin only declined one tick, from 30% to 29%. No mention of contract

cancellations, although they're probably saving that for tomorrow's call.

Nobody expected bad news for Q1 since Corona Virus was ramping in just the last month of the

quarter and reactions to such events on long-term rig lease contracts can stretch over many, many

months... if at all, if the event is brief.

Kinda surprised to see the stock off 3 cents after hours, but it was a helluva 2 day jump after all.

|

|

|

|

RIG

Apr 29, 2020 19:55:13 GMT -5

via mobile

Post by birdnest on Apr 29, 2020 19:55:13 GMT -5

How will this trade tomorrow?!?

|

|

Deleted

Deleted Member

Posts: 0

|

Post by Deleted on Apr 30, 2020 11:55:51 GMT -5

Part of an article I read this morning: : nice buy in the $0.80's mba. : I looked at Rig at $0.80 but I didn't feel cumfortable buying more. "One of the companies working with Exxon and Hess (HES) on that project is Transocean (RIG). The project is an important bulwark for Transocean, but it’s unlikely to generate warm feelings on Wall Street, which sees little hope for a rebound in the shares. Transocean’s debt levels are still a red flag for many investors, and there is no clear path to a major rebound in its rates. Before the 2014 oil-price downturn, the company was worth more than $15 billion. It now trades for less than $1 billion, and its adjusted operating earnings didn’t cover its interest expenses as of the end of last year, according to FactSet. “In a $70 world we thought Transocean, Valaris, Vallourec and Nabors needed new equity,” wrote Bernstein analyst Nicholas Green in a recent note, referring to the price of a barrel of oil, which currently sells for about $23. (Vallourec is a manufacturing company, but the other three drill offshore). “They now face an existential challenge to persuade both debt and equity funding to support them. We fear the equity may be worth zero, and would not want to take the risk of recovery on these names. We recommend remaining shareholders exit now.” www.barrons.com/articles/most-offshore-oil-stocks-are-hurting-these-2-look-like-buys-51586543450?siteid=yhoof2&yptr=yahoo |

|

|

|

Post by Blitz on Apr 30, 2020 14:06:10 GMT -5

Yous pays your moneys and yous takes your chances...

Time will tell. I was crazy for buying LVS too.

|

|

|

|

RIG

Apr 30, 2020 15:07:58 GMT -5

via mobile

birdnest likes this

Post by Blitz on Apr 30, 2020 15:07:58 GMT -5

How will this trade tomorrow?!? My crystal ball gives me 20/20 vision when I look in the rear view mirror... it shows 🟩↗️ 😎 |

|

|

|

Post by bjspokanimal on Apr 30, 2020 15:53:29 GMT -5

Good conference call this morning.

Most notable to me: The company's fleet is fully utilized, albiet at dayrates that allow

the company to be EBITDA positive, but EPS negative. Also, when asked if the company will

need to draw on it's revolving line of credit, the answer was that there would be no need

to draw on it anytime between now and the end of 2021.

They also alluded to indications that around 50, "floater" drilling rigs would likely be

retired in the industry over the next couple of years baring a big spike in oil prices. None

of the retirements would be from Transocean's fleet. It was a positive, owing to a

reduction in industry rig supply, given that almost nobody aside from Transocean is currently

building any new drillships.

|

|

|

|

RIG

May 1, 2020 12:24:26 GMT -5

Blitz likes this

Post by bjspokanimal on May 1, 2020 12:24:26 GMT -5

A little more color on the CC...

While the CEO stated that Transocean is not seeing contract cancellations like some of

the other drillers, they ARE seeing the work getting stretched and extended to some degree.

That appears to be for a couple of reasons:

1. Transocean's cancellation provisions are more stringent than other, smaller (eg: all of them)

drillers so it's more costly for an E&P company to cancel an agreement. So, if you're Exxon or

Chevron and you've got a choice between shutting in a big pile of shale wells for the cost of

doing the shut-ins or cancelling an 8 month drilling contract with Transocean for $20 million

instead of drilling away for 8 months with the $50 million lease cost of the rig, the choice is

easy. In this example, they're essentially saving 40% off the cost of using the rig by not

cancelling the contract and remember... ultra-deep water rigs are going for barely 40% of the

rate they go for during boom times these days ANYWAY.

2. Cancelling a contract on a Transocean rig risks not being able to get a rig to replace it with

the desired specifications later on after oil prices recover. The problems that other, smaller

drillers are experiencing is cutting into maintenance and safety expenditures that Transocean is

emphasizing to the oil majors and those majors know that Transocean's highest-specification rigs

are still almost fully contracted out, albeit at dayrates that lose money but are, collectively,

significantly EBITDA positive.

Transocean stated that they realistically expect to see some idle rigs this fall if oil prices stay

too low and one, mid-water semi-submersible called the 712 may be scrapped rather than upgraded. To the

extent rigs become idle, Thigpen said that they'll be much more assertive with cold-stacking them rather

than warm-stacking them in order to optimize cost control. This seemed to go hand in hand with their

assertion that they wouldn't need to tap their bank revolver between now and year end 2021.

One of the salient points they made when they suggested that upwards of 50 of their competitors'

rigs could be retired in the near future, was that it's costly to re-activate a cold-stacked rig that

is old and needs expensive upgrades in order to secure a contract. Most drillers just don't have the money to

do that when they're focused on just trying to stay alive these days. During boom times, that's no

problem, and upgrades of older rigs happen all the time.

For investors considering where a company like RIG will be a couple of years from now, that was a

pretty key point. Even if oil prices only recover to the same $55 to $70 range they were at before

corona virus began, if the global fleet of deep and ultra-deep floaters is significantly culled by then,

then a recovery in day rates could well be in the offing even without a prerequisite oil boom.

One final point. Transocean CEO Jeremy Thigpen was hired by Transocean (previously a VP at Varco) in

2015 while the current, long-duration oil slump was at it's deepest. Thigpen came in with no baggage and

a free hand to significantly re-make the company for long-term viability. The selloff and retirement of older

jackups and 3rd and 4th generation floaters was substantial, the strengthening of the balance sheet was

meaningful, and a couple of small acquisitions and 7th generation new-builds re-established the company

as the industry leader in ultra-deep and harsh environment drilling. In that regard, Transocean is a lot like

LVS, as LVS is only willing to enter the most lucrative markets with the most iconic integrated resorts.

Thigpen's reorganization results not only give me confidence in Transocean's ability to work through the

current industry crisis, but it was also a timely time to administer that kind of pain and agony on a company,

given that nobody knew the virus was coming but anybody who happened to be ready for it, rather than the

ongoing recovery that was happening in the drilling industry before the virus ever got her, essentially snagged

a significant competitive advantage that will hopefully become most apparent during the next industry

recovery.

|

|

|

|

RIG

May 1, 2020 13:50:26 GMT -5

Post by Blitz on May 1, 2020 13:50:26 GMT -5

I like that it appears they have adequate funds to weather the storm. They also have 80 projects good for 90 rig years. Chevron and Shell are keeping their rigs running too. Chevron is still spend $14B for this year's CapEx*. Exxon said this: Exxon reiterated cuts announced last month, when management said it sees 2020 capital spending of $23 billion, down from an earlier estimate of $33 billion, with the largest of the capital spending cuts in the Permian Basin.** So, even those are big cuts these giants are still spending... * seekingalpha.com/news/3567543-chevron-to-cut-2020-capex-another-2b-sees-operating-costs-down-1b** www.investors.com/news/chevron-earnings-exxon-earnings-q1-2020-oil-prices/From their conference call: Excerpt: When we look out over the next 18 months, we now see more than 80 projects with a total duration of almost 90 rig years. Excerpt: We are ending the first quarter with total liquidity of approximately $3 billion. Including unrestricted cash and cash equivalence of $1.5 billion and approximately $200 million of restricted cash dedicated for debt service and $1.3 billion from undrawn revolving credit facility. //////////////////////////// Excerpt: Turning now to our projected liquidity at December 31, 2021. Including our undrawn revolving credit facility and the potential securitization of the Deepwater Titan, our end of year 2021 liquidity is estimated to be between $1.2 billion and $1.4 billion. This liquidity forecast includes an estimated 2020 CapEx of $840 million as discussed previously and a reduced 2021 CapEx expectation of $815 million. The 2021 CapEx includes $750 million related to newbuilds and $65 million for maintenance CapEx. Please note that our CapEx guidance excludes any speculative reactivations or upgrades. seekingalpha.com/article/4341702-transocean-ltd-rig-ceo-jeremy-thigpen-on-q1-2020-results-earnings-call-transcript?part=single |

|

|

|

RIG

May 1, 2020 14:48:02 GMT -5

Blitz likes this

Post by bjspokanimal on May 1, 2020 14:48:02 GMT -5

Here is a site where one can monitor the trends in rig utilization and dayrates for the 3, primary rig types. Obviously, it's a lagged reading... stats thru February currently. The most current stats are for paid subscribers. ihsmarkit.com/products/oil-gas-drilling-rigs-offshore-day-rates.htmlFor comparative purposes, during peak times in recent oil cycles, the highest spec. drillships were contracting at over $600,000 a day and the highest spec. semi-submersibles were in the $525k to $550k range. I'm sure they're hoping that Titan can fetch close to $300k when that ship launches at year end as the best, 7th generation rig on the planet. |

|

... you've defined your total risk to be around $1 buck. So, I'm telling you, there's a chance at a multi-bagger ...

... you've defined your total risk to be around $1 buck. So, I'm telling you, there's a chance at a multi-bagger ...